Write Good Markets

The quality of a market determines whether it can resolve cleanly. A well-written market gives participants a clear question to predict, unambiguous outcomes to choose from, and rules that make the final result straightforward to determine. A poorly written market creates confusion at settlement — and confused settlements lead to disputes.

This page covers the practical decisions that separate a market that resolves well from one that doesn't.

Writing a clear question

The question is the center of the market. Everything else — the outcomes, the rules, the timing — exists to answer it cleanly.

A good question is:

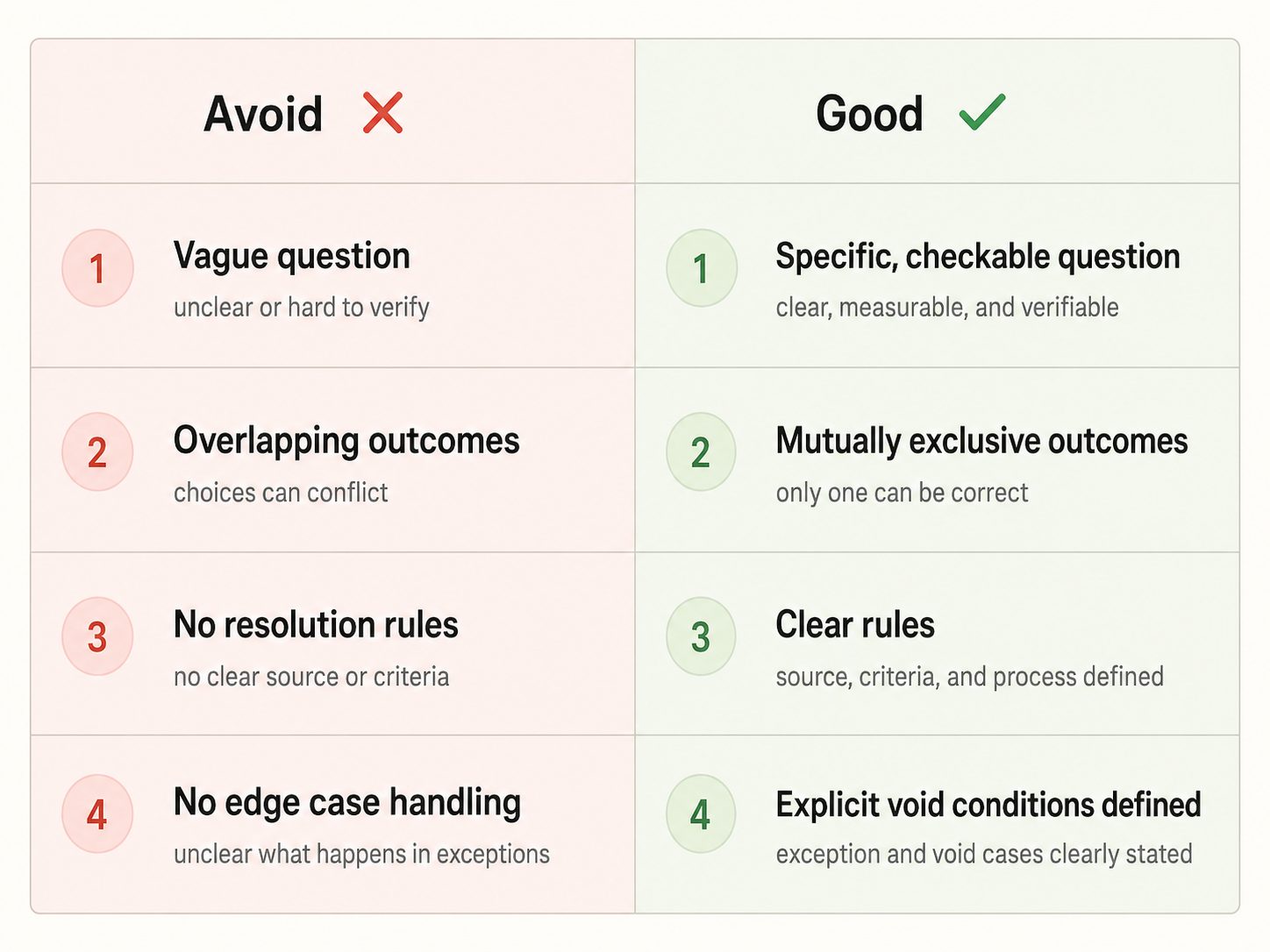

- Specific. It refers to a defined event, not a broad topic. "Will the match on June 12 end in a draw?" is specific. "Who will win the league?" without a defined league and season is not.

- Verifiable. The answer must be checkable against reality. If you cannot point to a source or event that will definitively tell you the result, the question is not ready to become a market.

- Singular. Each question should have exactly one thing being predicted. Combining two questions into one ("Will X happen and will Y happen?") makes the outcome structure ambiguous.

- Time-bound. The question should imply or explicitly state the deadline by which the event either happens or doesn't. Open-ended questions invite open-ended disputes.

- Genuinely uncertain. A good market question needs both sides to have a reason to participate. If the answer is obvious to most people, the market will lack liquidity and the prediction itself loses meaning. The question should be designed so that participants with different views can each reasonably choose either side.

Designing outcomes

Outcomes are what participants choose between. They need to do two things simultaneously: cover every possible result, and never overlap.

Cover every possibility. If a real-world result could occur that doesn't fit any of the listed outcomes, the market has a structural problem. Think through edge cases before publishing. If there is a reasonable scenario where none of your outcomes apply, you need an additional outcome — or a clearer question.

Never overlap. If a result could plausibly fit more than one outcome, participants will disagree about how it should be interpreted. Outcomes should be mutually exclusive. "Team A wins" and "Team A wins by more than two goals" cannot both be options in the same market.

Be self-explanatory. Each outcome label should be clear on its own, without requiring participants to read the rules to understand what it means. If you find yourself writing long rules to explain what an outcome label means, the label itself needs to be rewritten.

Writing rules

Rules are the settlement standard. When the event occurs and it is time to determine the result, the creator — and any disputant or arbitrator — will refer to the rules.

Good rules answer three questions:

What exactly counts? Define the conditions for each outcome precisely. If your question is about a vote passing, specify what threshold counts as passing, what body is voting, and by what deadline.

What source will be used? Name the reference standard you will rely on. An official announcement, a specific data provider, a verified broadcast result. Vague sourcing creates room for disagreement when the result is close or contested.

What happens in edge cases? Every market has potential edge cases: the event is postponed, cancelled, or ends in a technical result that doesn't fit the outcomes as written. Rules should state explicitly how these cases are handled — and whether such a scenario should void the market.

Rules do not need to be long. They need to be complete. A one-paragraph set of rules that covers the key scenarios is better than three paragraphs that leave the hard cases unanswered.

Common mistakes

The question is too broad. "Will crypto recover this year?" cannot resolve cleanly. There is no defined event, no measurable threshold, no specific asset.

Outcomes leave gaps. If the only options are "Yes" and "No" but the real-world result is "delayed indefinitely," neither outcome applies. Add a third outcome or define how that scenario is handled in the rules.

Outcomes overlap. Two outcomes that could both describe the same result will produce a dispute almost every time.

The rules don't name a source. Saying "the result will be determined by the official result" without specifying which official source leaves room for conflicting interpretations.

Edge cases are ignored. The market is built around the expected scenario and nothing else. One unexpected outcome later, and the rules provide no guidance.

The settlement test

Before publishing, apply one final check: if the event happens tomorrow, could you settle this market clearly, quickly, and without needing to make judgment calls that go beyond what the rules say?

If the answer is yes, the market is ready. If you find yourself hesitating, revise before publishing.

Topic suitability

Not all topics are equally suited to prediction markets.

Sports events, weather and everyday life predictions, entertainment outcomes like release dates and award results, and product or software launches are naturally well-suited topic types. These events have defined endpoints, results that can be verified through public sources, and participants who can reasonably take either side.

Crypto asset prices and macroeconomic data require more care. Prices move quickly, and a question that is even slightly imprecise can easily generate disputes. Macro data such as GDP or CPI figures may be revised after initial publication, adding complexity to settlement. Markets in these areas are not off-limits, but creators need to address these variables in the rules from the start.

Some topics should be avoided entirely. Predictions that involve personal privacy, or markets that resolve on disaster casualty counts, are not appropriate to frame as prediction mechanisms. Highly politically sensitive topics and ongoing legal proceedings are likely to produce irreconcilable disagreements about the result even with clear rules. These topics should not be published as prediction markets.